California Advocacy UPdate – April 2026

It’s been a busy year for our Advocacy and Action team in California so far. We helped shape the findings of a Commissioner’s Smoke Damage and Insurance Task Force as an appointed member, contributed to an important victory in a water damage claim denial case, and are actively supporting 18 pending legislative proposals. We’re coordinating with lawmakers and Committee staffers, negotiating on amendments and bringing the experienced and knowledgeable voice that’s earned us a place at the table when decisions are being made that impact insurance consumers and disaster survivors.

UP Executive Director Amy Bach was a lead witness at a Senate Insurance Committee hearing on April 8th at the request of California’s Insurance Commissioner.

Increased premiums, non-renewals, and post-wildfire underinsurance and claim frustrations have spurred the introduction of a record number of legislative reform proposals in California this session and we’re helping refine and advance a number of them:

- Enacting reforms to relieve extra pain points in the disaster recovery insurance claim process

- Establishing standards for testing and remediating toxic wildfire debris in smoke-damaged homes

- Strengthening the CA FAIR Plan to better serve California property owners

- Extending non-renewal moratoriums after disasters

- Increasing wildfire risk reduction by funding a county-level wildfire mitigation coordinator program.

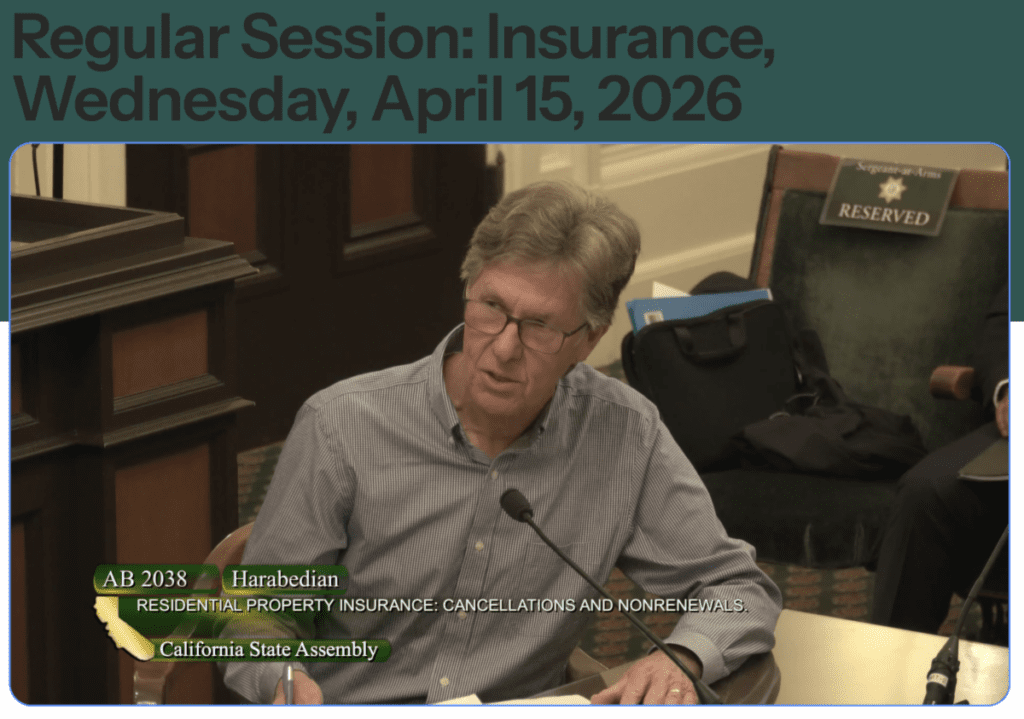

UP Program Specialist and former CDI Deputy Commissioner, Joel Laucher testified in the Capitol on April 15th in support of extending non-renewal moratoriums after wildfires

Our advocacy efforts and positions are informed by the work we do directly with consumers, our decades of monitoring and guiding people through insurance sales and claims processes and the data we gather through pre and post-disaster surveys through our Roadmap to Preparedness and Roadmap to Recovery(r) Programs. Our most recovery recent survey captured data from insured Los Angeles Wildfire Survivors 12 months after the fires.

We refine our survey questions and data analysis in consultation with experts affiliated with Boise State University, CalWestern Law School and Stanford University to ensure the integrity of our results. Los Angeles became the 14th fire-affected community to join this project. You can view this recent report, summary data and significant findings at: www.uphelp.org/surveyresults.

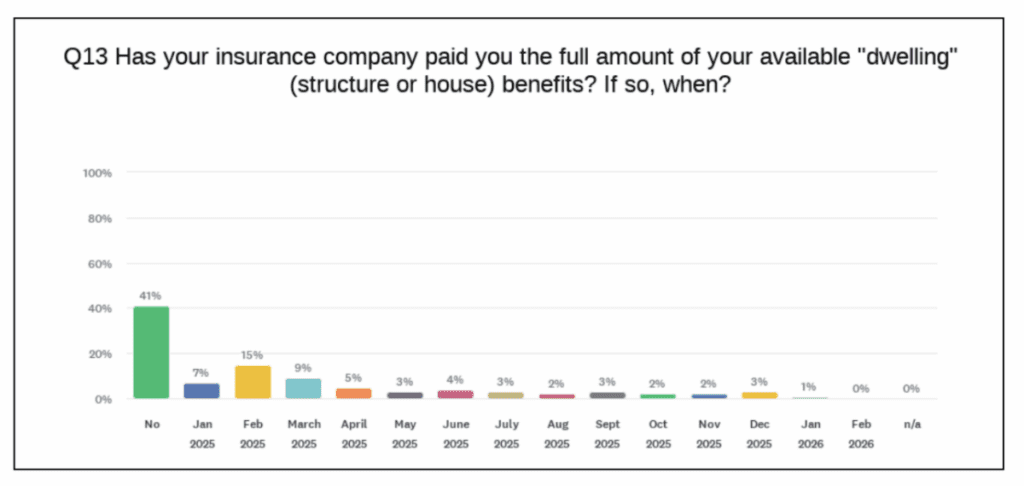

Survey results from our 2025 LA Wildfires 12 Month Survey show 41% of total loss survey respondents have not yet settled the dwelling portion of their claim. The graph above shows no “peak” in the recovery, rather a slow, continual rate of settling. This is a common attribute of post-disaster insurance recovery.

A substantial number, 69%, of households report being underinsured by an average amount of $247 per square foot. The dollar amount is a significant increase from underinsurance data we have collected from previous wildfires recovery surveys. Notably, 24% of survey participants reported after 12 months, they do not yet know if they are underinsured. UP will continue to monitor this subset in our future surveys because it is an indicator of a much higher rate of underinsurance.

A hot ticket: The Insurance Commissioner race

This year’s race for California’s Insurance Commissioner has drawn more media and public attention than any previous election for this position…by a long shot. An historic number of candidates are vying for this challenging job, and the stakes couldn’t be higher for the consumers UP serves, not to mention California taxpayers, real estate sales and values and the larger financial ecosystems that property insurance touches.

If you are interested in hearing directly from the candidates, here are a few opportunities between now and the June 2nd primary election:

UP is partnering with the non-profit CERES during SF Climate Week to host a California Insurance Commissioner Candidate Forum in San Francisco on April 22nd. You can watch the recording here.

Then in May, Executive Director Amy Bach will be moderating an Insurance Commissioner Candidates forum in Santa Monica.

While UP does not endorse candidates for public office, we’re in touch with the leading candidates and are committed to working productively with whoever prevails. The next Commissioner will have to be up to the challenge of the brutal balancing act of restoring availability and affordability while holding insurers accountable at claim time.

Two additional opportunities to meet the candidates:

- April 29th at 5:30pm – Virtual Forum hosted by the League of Women Voters

- May 7th at 7pm – In person at the NAACP Pasadena Candidates Forum on at Loma Alta Park Gymnasium.

UP Working Groups are on the case…

The underlying causes of the insurance affordability and availability crisis include climate change, inflation and sophisticated risk modeling/AI and they can’t be solved with a magic wand or just one piece of legislation. But by convening subject matter experts, stakeholders, researchers and community leaders and parsing issues bite by bite, UP is advancing solutions in meaningful ways through two working groups and related initiatives.

We want to take a moment to thank the hundreds of members (you know who you are) of one of our hardest working, working groups: our “WRAP” group (Wildfire Risk Reduction and Asset Protection).

The WRAP group has been meeting monthly for years and has scored some impressive wins:

- Helped establish official standards for effective wildfire risk reduction

- Supported the CDI in adopting regulations that require insurers to adjust their rates to reward risk-reduced properties and communities.

- Connected several insurers with pro-active risk reduction communities, which led to them making significant commitments to insure more homes.

- Built an online county-by-county resource center to connect consumers with mitigation help programs in their area.

- Ongoing monitoring of pricing and availability in the marketplace through consumer surveys and agent/broker communications.

- Educating the public on current strategies for keeping insurance affordable, staying insured and reducing risk through consumer-facing education and shopping help events, in-person and online throughout the year.

We continue to work toward more meaningful discounts and renewal assurances and big picture solutions. We know consumers are not yet feeling relief from these efforts, and marketplace dynamics in our current era are fraught.

Our Insurance Alternatives Working Group is identifying models of non-profit, captive and self-insured risk pools that may be options for HOAs and some communities. Most recently, the group heard an innovative proposal on “How Group Homeowners Insurance Could Promote Climate Adaptation and Resilience”.

Thank you to our funders, partners and stakeholders for moving these efforts forward…Onward and UPward!

This year we are celebrating 35 years of impactful work!

Make a donation today to support the nonprofit that has your back when insurance matters!